Sensitivity Analysis of Value-at-Risk and Expected Shortfall to Copula Misspecification in CGMY Jump-Diffusion Models

DOI:

https://doi.org/10.33003/fjs-2026-1008-5333Keywords:

Value-at-Risk, Expected Shortfall, Copula Misspecification, CGMY Jump-Diffusion, Model Risk, Basel III, Risk ManagementAbstract

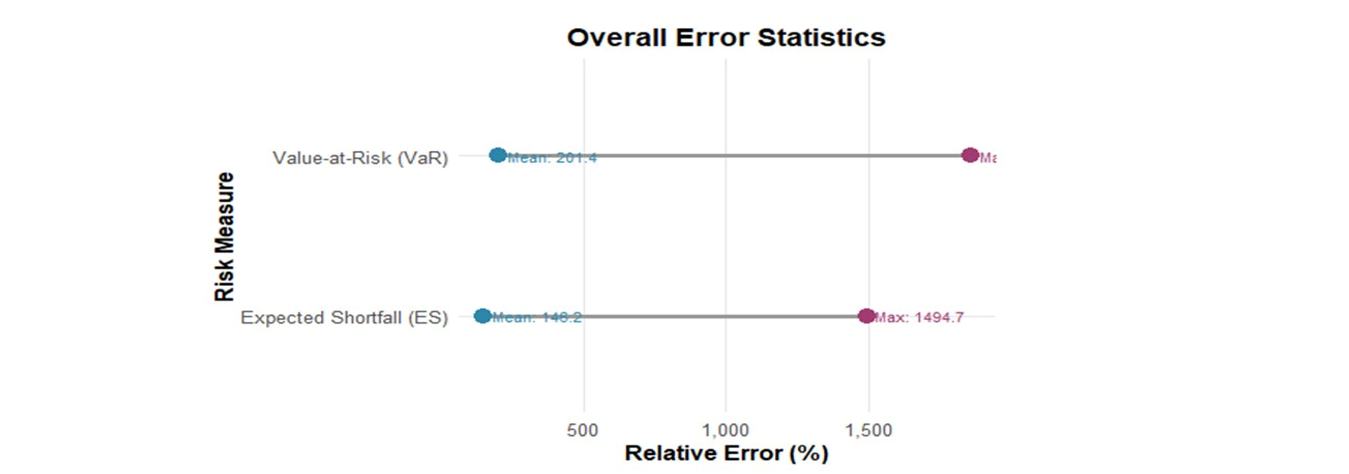

This study provides a comprehensive sensitivity analysis of risk measures to copula misspecification in CGMY jump-diffusion models, revealing substantial vulnerabilities in Value-at-Risk (VaR) and Expected Shortfall (ES) calculations. Using Monte Carlo simulation with 10,000 paths per scenario across multiple volatility regimes, jump intensities, and confidence levels, the study demonstrates that mean relative errors exceed 200% for VaR and 146% for ES when averaging across all six copula families including the severely misspecified Gumbel copula. Crucially, well-specified elliptical copulas exhibit bootstrap mean errors of only 1.5–2.3% for VaR and 2.0–2.3% for ES, while the Gumbel copula alone drives errors to 280.6% for VaR and 238.4% for ES in bootstrap-estimated means (corresponding to 1,190% and 839% in the worst individual scenarios), indicating that the aggregate averages are dominated by a single family’s structural failure rather than a pervasive property of the modelling framework. Two-way ANOVA confirms that both copula family (F = 3,614 for VaR; F = 5,192 for ES) and confidence level (F = 66 for VaR; F = 44 for ES) exert highly significant effects (all p < 2×10⁻¹⁰), while Tukey HSD post-hoc tests demonstrate that the Gumbel copula is the sole source of statistically distinguishable pairwise differences all five non-Gumbel copulas are statistically indistinguishable from one another at the 95% family-wise level. Contrary to expectation, low-volatility regimes exhibit the highest sensitivity to copula misspecification, while severe-jump regimes exhibit the lowest.

References

Boucher, C. M., Daníelsson, J., Kouontchou, P. S., & Maillet, B. B. (2014). Risk models-at- risk, Journal of Banking & Finance, 44, 72-92.

Brechmann, E. C., & Czado, C. (2013). Risk management with high-dimensional vine copulas: An analysis of the Euro Stoxx 50, Statistics & Risk Modeling, 30(4), 307-342.

Carr, P., Geman, H., Madan, D. B., & Yor, M. (2002). The fine structure of asset returns: An empiricalinvestigation.JournalofBusiness,75(2),305-332. https://doi.org/10.1086/339036

Cerrato, M., Crosby, J., Kim, M., & Zhao, Y. (2017). Modeling credit spreads with time-varying jump risks and jumps in returns. Journal of Banking & Finance, 83, 119-134.

Demarta, S., & McNeil, A. J. (2005). The t copula and related copulas, International Statistical Review, 73(1), 111-129.

Derman, E. (2011). Models behaving badly: Why confusing illusion with reality can lead to disaster, on Wall Street and in life, Free Press.

Dewick, P., & Liu, S. (2022). Copula modelling to analyse financial data. Journal of Risk and Financial Management, 15(3), Article 104. https://doi.org/10.3390/jrfm15030104

Embrechts, P., Lindskog, F., & McNeil, A. (2003). Modelling dependence with copulas and applications to risk management, Handbook of Heavy Tailed Distributions in Finance, 8(1), 329-384.

Engle, R. F. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models, Journal of Business & Economic Statistics, 20(3), 339-350.

MacKenzie, D., & Spears, T. (2014). 'The formula that killed Wall Street': The Gaussian copula and modelling practices in investment banking. Social Studies of Science, 44(3), 393- 417.

McNeil, A. J., Frey, R., & Embrechts, P. (2005). Quantitative risk management: Concepts, techniques and tools. Princeton University Press.

Merton, R. C. (1976). Option Pricing When Underlying Stock Returns Are Discontinuous, Journal of Financial Economics, 3(1-2), 125-144. (https://www.sciencedirect.com/science/article/abs/pii/0304405X76900296)

Nthiwa, K., Kube, M., & Cyprian, A. (2023). A Jump Diffusion Model with Fast Mean- Reverting Stochastic Volatility, Discrete Dynamics in Nature and Society, 11(2), 45- 67. (https://doi.org/10.1155/2023/2746415)

Ornthanalai, C. (2014). Lévy jump risk: Evidence from options and returns, Journal of Financial Economics, 112(1), 69-90.

Patton, A. J. (2006). Modelling asymmetric exchange rate dependence, International Economic Review, 47(2), 527-556.

Sklar, M. (1959). Fonctions de répartition à n dimensions et leurs marges. Publications de l'Institut de Statistique de l'Université de Paris, 8, 229-231.

Zhang, S., Okhrin, O., Zhou, Q. M., & Song, P. X.-K. (2013). Goodness-of-fit test for specification of semiparametric copula dependence models. Economic Risk Berlin, 649

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 Abdulmudallib Ibrahim Abdul, Adesupo Akinrefon, Okolo Abraham, Emmanuel Torsen

This work is licensed under a Creative Commons Attribution 4.0 International License.