ROBUSTNESS CHECKS AND SENSITIVITY ANALYSIS OF ECONOMETRIC MODELS USING SIMULATED SYNTHETIC DATA: REPLICATING THE STATISTICAL PROPERTIES OF NIGERIAN MACROECONOMIC VARIABLES

DOI:

https://doi.org/10.33003/fjs-2026-1005-4822Keywords:

Monte Carlo Simulation, Economic Growth, ARDL, VECM, FMOLS, CointegrationAbstract

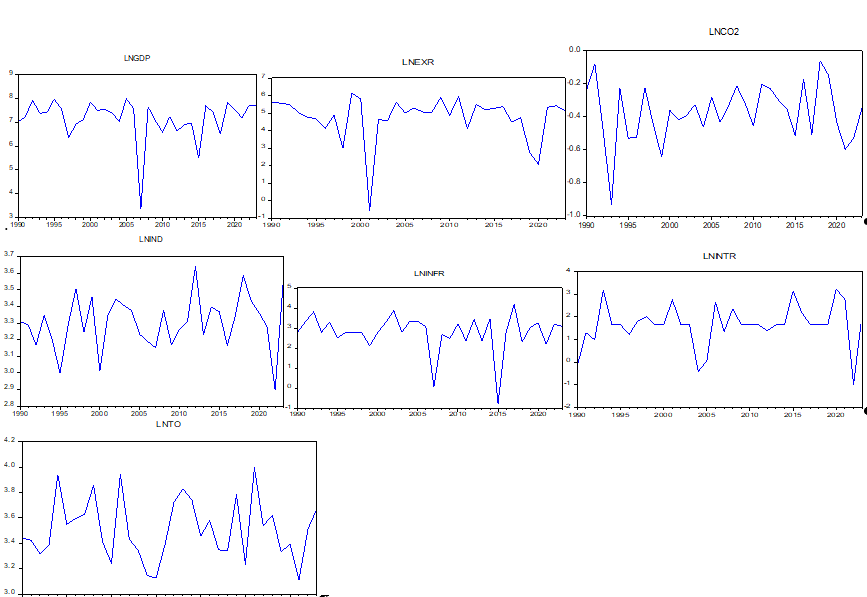

This study applies a Monte Carlo simulation approach to assess the robustness of macroeconomic growth models in Nigeria from 1990 to 2023 by generating 33 synthetic datasets that mimic the statistical behavior and interrelationships of key variables such as GDP, exchange rate, inflation, interest rate, industrialization, carbon emissions, and trade openness. Using parameters derived from time-series models like VAR, the simulated data preserve essential features including mean, variance, autocorrelation, and long-run relationships, enabling detailed sensitivity analysis. The findings show that log transformation generally stabilizes variance, although GDP, exchange rate, and inflation still exhibit skewness and heavy-tailed distributions, indicating persistent economic volatility. Stationarity tests confirm that all transformed variables are stable at levels. Long-run estimation using FMOLS reveals that inflation and interest rates positively influence GDP, while industrialization negatively affects growth, suggesting structural inefficiencies; other variables show limited long-run impact. Short-run dynamics from ARDL models highlight cyclical GDP adjustments, negative effects of exchange rate depreciation, and unstable trade openness impacts, alongside complex lag interactions among variables. Cointegration tests confirm stable long-run relationships, and VECM results indicate that, over time, industrialization, trade openness, carbon emissions, and inflation promote growth, whereas exchange rate depreciation and high interest rates hinder it, with short-run fluctuations largely driven by monetary and price adjustments.

References

Adenomon, M. O., Ojo, J. A., & Ojehomon, V. E. T. (2020). A time series analysis of the impact of COVID-19 pandemic on the Nigerian stock market returns. Asian Journal of Probability and Statistics, 6(4), 1–17.

Adeoye, B. W., Aremo, A. G., & Ogunjimi, J. A. (2021). Macroeconomic variables and economic growth in Nigeria: A robustness and sensitivity analysis. Journal of Economics and Sustainable Development, 12(18), 1-11.

Carriero, A., Clark, T. E., & Marcellino, M. (2022). Proxy vector autoregressions in a data-rich environment. Journal of Econometrics, 228(2), 326–348.

Chan, J. C. C. (2022). Comparing point and density forecasts: A new methodology. International Economic Review, 63(3), 1087–1112.

Doornik, J. A., & O’Brien, R. J. (2020). Numerically stable and accurate statistical computation via matrix decomposition and simulation. Journal of Econometrics, 217(1), 1–18.

Goulet Coulombe, P. (2023). The macroeconomy and the yield curve: A dynamic latent factor approach. Journal of Applied Econometrics, 38(2), 199–221.

Goulet Coulombe, P., Leroux, M., Stevanovic, D., & Surprenant, S. (2022). How is machine learning useful for macroeconomic forecasting? Journal of Applied Econometrics, 37(5), 920–964.

Huber, M., Lafférs, L., & Mellace, G. (2020). A bootstrap t-test for synthetic control methods. Journal of Applied Econometrics, 35(7), 926–935.

Hendry, D. F. (1984). Monte Carlo experimentation in econometrics. In Z. Griliches & M. D. Intriligator (Eds.), Handbook of econometrics (Vol. 2, pp. 937–976). Elsevier.

Kremer, M., Bickenbach, F., Lührmann, M., & Nosenko, D. (2022). Using synthetic data to evaluate the causal impact of shocks. Journal of Economic Dynamics and Control, 135, 104321.

Lenza, M., & Primiceri, G. E. (2022). How to estimate a vector autoregression after March 2020? Journal of Applied Econometrics, 37(4), 688–699.

Lewis, M. A., Hsu, J. S., & Bohidar, N. (2020). Sensitivity analysis for unmeasured confounding in meta-analyses. Journal of the American Statistical Association, 115(531), 1077–1088.

Leamer, E. E. (1983). Let's take the con out of econometrics. The American Economic Review, 73(1), 31–43.

Plagborg-Møller, M., & Wolf, C. K. (2021). Local projections and VARs estimate the same impulse responses. Econometrica, 89(2), 955–980.

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 Monday Osagie Adenomon, Mary Unekwu Adehi, Mahmud Musa Salisu, Nweze Obina Nweze

This work is licensed under a Creative Commons Attribution 4.0 International License.