Symmetric Garch Modeling of Some Cryptocurrency Returns: Implications for Coin Investment Decision-Making

DOI:

https://doi.org/10.33003/fjs-2026-1009-4760Keywords:

Digital Coin, GARCH Modeling, Mean Reversion, Fat-Tails, Short-and Long-Term Investments, NigeriaAbstract

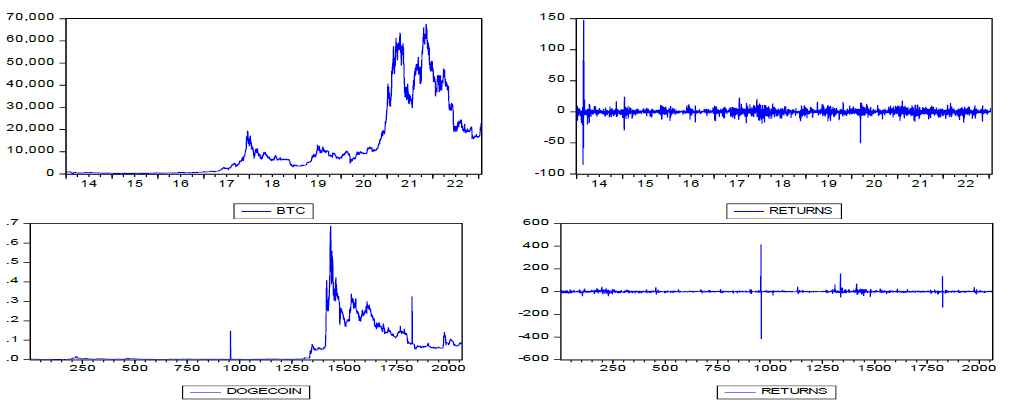

The rapid growth of cryptocurrency markets has intensified interest in understanding the volatility dynamics of digital assets due to their implications for investment decision-making, risk management, and financial forecasting. Although numerous studies have examined cryptocurrency volatility using GARCH-type models, limited attention has been given to the comparative analysis of volatility mean reversion and half-life measures across multiple cryptocurrencies and their implications for investment horizons. This study addresses this gap by investigating the volatility behaviour, persistence, mean reversion, and volatility half-lives of eight major cryptocurrencies, namely Bitcoin (BTC), Dogecoin (DOGE), Ethereum (ETH), Litecoin (LTC), Tether (USDT), Stellar (XLM), Monero (XMR), and Ripple (XRP) using daily closing price data from January 2014 to August 2024. Descriptive statistics, unit root tests, ARCH effect tests, and symmetric GARCH (1,1) models were employed to estimate volatility persistence and compute volatility half-life measures. The results revealed that all cryptocurrency return series exhibited non-normal and leptokurtic distributions, significant ARCH effects, and strong volatility clustering. The estimated GARCH models indicated high volatility persistence across all cryptocurrencies, with persistence coefficients ranging from approximately 0.8706 for USDT to 0.99995 for BTC. The computed volatility half-lives varied substantially, ranging from 5 days for USDT and 12 days for ETH to 1,708 days for XRP and 13,864 days for BTC, indicating marked differences in the speed of adjustment to market shocks. Cryptocurrencies with shorter volatility half-lives, such as USDT and ETH, were found to be more suitable for short-term trading strategies, whereas BTC and XRP exhibited characteristics consistent with longer-term investment horizons.

References

Aalborg, H. A., Molnar, P., and De Vries, J. E. (2019). What Can Explain the Price, Volatility and Trading Volume of Bitcoin? Finance Research Letters, 29, 255-265.

Ahmed, R. R., Vveinhardt, J., Streimikiene, D., and Channar, Z. A. (2018). Mean Reversion in International Markets: Evidence from GARCH and Half-Life Volatility Models, Economic Research-Ekonomska Istraživanja, 31(1), 1198-1217.

Agyarko, K., Buabeng, A., and Acquah, J. (2019). Modeling the Volatility of the Price Of Bitcoin. American Journal of Mathematics and Statistics, 9(4), 151-159.

Alrabadi, D. W. H. (2018). Dynamic Mean Reversion of Stock Prices: Evidence from Amman Stock Exchange. Jordan Journal of Economic Sciences, 5(1), 57-65.

Belliler, S. and Yildirim, T. (2021a). Volatility and Return Behaviour of Bitcoin as a Financial Investment Tool. International Journal of Financial Studies, 9(1), 123-136.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307–327.

Corbet, S., Meegan, A., Larkin, C., Lucey, B., and Yarovaya, L. (2018). Exploring the Dynamic Relationships Between Cryptocurrencies and Other Financial Assets. Economics Letters, 165, 28-34.

Cortese, F. P., Kolm, P. N., and Lindström, L. (2023). What Drives Cryptocurrency Returns? A Sparse Statistical Jump Model Approach. Digital Finance, 5, 483-518.

David, S. A., Inacio, C. M. C., Nunes, R., and Machado, J. A. T. (2021). Fractional and Fractal Processes Applied to Cryptocurrencies Price Series. Journal of Advanced Research, 32, 85-98.

Dickey, D. A., and Fuller, W. A. (1979). Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association, 74(366), 427-431.

Engle, R. F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of UK inflation. Econometrica, 55(4), 324–356.

Etienne, H., Charbel, B., Talie, K., and Roland, B. (2022). Volatility Interdependence Between Cryptocurrencies, Equity, and Bond Markets. Computational Economics, 112(1), 432-448.

Gbenro, N. and Moussa, R. K. (2019). Asymmetric Mean Reversion in Low Liquid Markets: Evidence from BRVM. Journal of Risk and Financial Management, 12(38), 1-19.

Greene, W. H. (2010). Econometric Analysis (7th ed.). Upper Saddle River, NJ: Prentice Hall.

Hamed, G., Mohammad, M., and Nima, R. (2021). Asymmetric Bitcoin Volatility under Structural Breaks. Digital Finance, 20(21), 44-59.

Han, Y. H. (2019). Long Memory Volatility and Bernoulli Jumps in Daily Cryptocurrency Prices. Journal of Financial Studies, 8, 109-138.

Huang, J. Z., Huang, Z. J., and Xu, L. (2021). Sequential Learning of Cryptocurrency Volatility Dynamics: Evidence Based on a Stochastic Volatility Model with Jumps in Returns and Volatility. The Quarterly Journal of Finance, 11(2), 147-158.

Huthaifa, A., Alaa, A. A., and Ahmad, A. (2020). Modeling and Forecasting the Volatility of Cryptocurrencies: A Comparison of Nonlinear GARCH-Type Models. International Journal of Financial Research, 11(4), 346-356.

Jarque, A. K. & Bera, C. M. (1980). Efficient tests for normality, homoskedasticity and serial independence of regression residuals. Economics Letters, 6, 255-259.

Jarque, C. M., & Bera, A. K. (1987). A test for normality of observations and regression residuals. International Statistical Review, 55(2), 163-172.

Jimoh, S. O. and Oluwasegun, O. B. (2020). The Effect of Cryptocurrency Returns Volatility on Stock Prices and Exchange Rate Returns Volatility in Nigeria. Financial Economics, 16(6), 352-365.

Jinan, L., and Apostolos, S. (2019).Volatility in the Cryptocurrency Market. International Conference on Applied Economics, 4(3), 1-41.

John, A., Logubayom, A. I., and Nero, R. (2019). Half-Life Volatility Measure of the Returns of Some Cryptocurrencies. Journal of Financial Risk Management, 8, 15-28.

Joseph, T. E., Jahanger, A., Onwe, J. C., and Balsalobre Lorente, D. (2024). The Implication of Cryptocurrency Volatility on Five Largest African Financial System Stability. Financial Innovation, 10(42), 1-19.

Karim, M. M., Hammoudeh, S., Ali, M. H., Yarovaya, L., and Uddin, M. H. (2023). Return-Volatility Relationships in Cryptocurrency Markets: Evidence from Asymmetric Quantiles and Non-Linear ARDL Approach. International Review of Financial Analysis, 90, 1-21.

Katsiampa, P. (2019). Volatility Estimation for Bitcoin: A Comparison of GARCH Models. Economics Letters, 158, 3-6.

Kim, J. M., Jun, C., and Lee, J. (2021). Forecasting the Volatility of the Cryptocurrency Market by GARCH and Stochastic Volatility. Mathematics, 9, 1-16.

Koutmos, D. (2018). Return and Volatility Spillovers among Cryptocurrencies. Economics Letters, 173, 122-127.

Kuhe, D. A. (2024). Rudiments of Applied Time Series Analysis. First Edition. Climax Publishers, Makurdi-Nigeria. Pp. 276-278.

Kuhe, D. A., & Audu, S. D. (2016). Modeling volatility mean reversion in stock market price: Implication for long-term investment. Nigerian Journal of Scientific Research, 15(1), 131-139.

Lee, S. S. and Wang, M. (2024). Variance Decomposition and Cryptocurrency Return Prediction. International Review of Financial Analysis, 69, 112-123.

Naimy, V. Y., and Hayek,.M. R. (2018). Modelling and predicting the Bitcoin Volatility using GARCH Models. International Journal of Mathematical Modelling and Numerical Optimization, 8(3), 24-38..

Pinar, K. S., Mustafa, O., Ozgur, C., and Ayca, A. (2020). Long Memory in the Volatility of Selected Cryptocurrencies: Bitcoin, Ethereum and Ripple. Journal of Risk and Financial Management, 13(6), 112-125.

Seabe, P. L., Moutsinga, C. R. B., and Pindza, E. (2024). Optimizing Cryptocurrency Returns: A Quantitative Study on Factor-Based Investing. Mathematics, 12, 1-28.

Salisu, A. A., Tiwari A. K., and Raheem, I. D. (2018). Analyzing the Distribution Properties of Bitcoin Returns. Econometric and Allied Research, 18(3), 45-59.

Schwarz, G. (1978). Estimating the dimension of a model. Annals of Statistics, 6(2), 461–464.

Swan, M. (2020). The Bitcoin Standard: The Decentralized Alternative to Central Banking. Wiley: Saifedean Ammous’s Book. Pp. 89-103.

Takaishi, T. (2021). Time-varying properties of Asymmetric Volatility and Multifractality in Bitcoin. PLoS ONE, 16(1), e0246209.

Wang, C. (2021). Different GARCH Models Analysis of Returns and Volatility in Bitcoin. Data Science in Finance and Economics, 1(1), 37-59.

Woebbeking, F. (2021). Cryptocurrency Volatility Markets. Digital Finance, 3, 273-298.

Yukun L., and Aleh, T. (2018). Risks and Returns of Cryptocurrency. International Journal of Academic Research in Business and Social Sciences, 4(5), 35-50.

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 David Adugh Kuhe, Amak Solomon Ayum, Tersoo Uba

This work is licensed under a Creative Commons Attribution 4.0 International License.