RUNGE–KUTTA DUAL ATTENTION OPTIMIZATION FOR LSTM-BASED FINANCIAL TIME-SERIES FORECASTING: STABILITY, EFFICIENCY, AND ROBUSTNESS

DOI:

https://doi.org/10.33003/fjs-2026-1003-4723Keywords:

Runge–Kutta Optimization, Dual-Attention LSTM, Hyperparameter Tuning, Genetic Algorithm (GA), Brown Bear Optimization Algorithm (BBOA), Hyperparameter optimization, Metaheuristic Optimization, Financial Volatility ForecastingAbstract

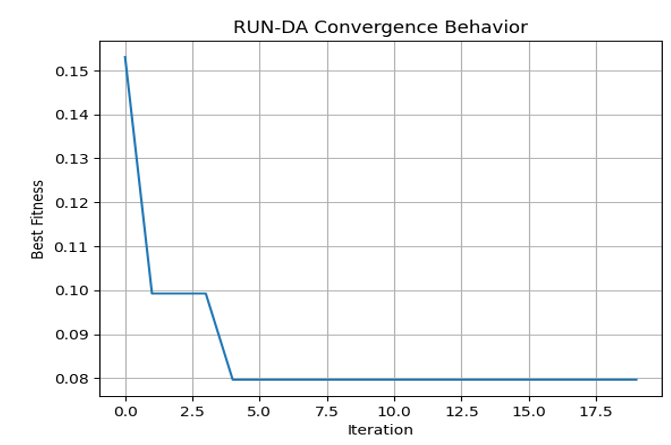

This study evaluates the performance of the Runge–Kutta Dual Attention (RUN-DA) optimization framework for hyperparameter tuning in a dual-attention Long Short-Term Memory (LSTM) model for financial time-series forecasting. The experiment was conducted using historical stock price data of MRS Oil Plc covering the period 2012–2024, representing a Nigerian financial market dataset. The proposed optimizer was compared with the Genetic Algorithm (GA) and Brown Bear Optimization Algorithm (BBOA) under consistent experimental conditions. Model performance was assessed using validation Mean Squared Error (MSE) and computational efficiency. Results show that RUN-DA achieved the lowest mean fitness value of 0.1369, compared with 0.4054 for GA and 0.1924 for BBOA. Sensitivity analysis indicated that moderate learning rates and time-step values produced more stable generalization performance. The evaluation under different market regimes further showed that RUN-DA maintained relatively lower fitness values across volatility conditions, decreasing from 0.2343 in low-volatility periods to 0.0473 in high-volatility periods, while GA and BBOA recorded higher corresponding values. In terms of computational efficiency, RUN-DA converged in 1015.23 seconds, slightly faster than GA (1073.25 seconds) and substantially faster than BBOA (2147.05 seconds). These results suggest that RUN-DA provides an effective optimization approach for improving LSTM-based financial forecasting models, although further validation on additional financial assets and evaluation metrics is recommended.

References

Bao, W., Yue, J., & Rao, Y. (2017). A deep learning framework for financial time series using

stacked autoencoders and long short-term memory. PLOS ONE, 12(7), e0180944. https://doi.org/10.1371/journal.pone.0180944.

Bhuiyan, M. S. M., Rafi, M. A., Rodrigues, G. N., Mir, M. N. H., Ishraq, A., Mridha, M. F., &

Shin, J. (2025). Deep learning for algorithmic trading: A systematic review of predictive models and optimization strategies. Array, 26, 100390. https://doi.org/10.1016/j.array.2025.100390.

Fischer, T., & Krauss, C. (2018). Deep learning with long short-term memory networks for

financial market predictions. European Journal of Operational Research, 270(2), 654–669. https://doi.org/10.1016/j.ejor.2017.11.054.

Fu, Y. (2025). Research on financial time series prediction model based on multifractal trend

cross correlation removal and deep learning. Procedia Computer Science, 261, 217–226. https://doi.org/10.1016/j.procs.2025.04.192

Ghazieh, L., & Chebana, N. (2021). The effectiveness of risk management system and firm

performance in the European context. Journal of Economics, Finance and Administrative Science, 26(52), 182–196. https://doi.org/10.1108/JEFAS-07-2019-0118

He, K, Yang, Q, Ji, L, Pan, J, & Zou, Y (2023). Financial time series forecasting with the

deep learning ensemble model. Mathematics, mdpi.com, https://www.mdpi.com/2227-7390/11/4/1054.

Hochreiter, S., & Schmidhuber, J. (1997). Long short-term memory. Neural Computation,

9(8), 1735–1780. https://doi.org/10.1162/neco.1997.9.8.1735.

Imran, M., Hashim, R., & Abd Khalid, N. E. (2013). An overview of particle swarm

optimization variants. Procedia Engineering, 53, 491–496. https://doi.org/10.1016/j.proeng.2013.02.063

Paulson, J. A., & Tsay, C. (2025). Bayesian optimization as a flexible and efficient design framework for sustainable process systems. Current Opinion in Green and Sustainable Chemistry, 51, 100983. https://doi.org/10.1016/j.cogsc.2024.100983

Prakash, T., Singh, P. P., Singh, V. P., & Singh, S. N. (2023). A Novel Brown-bear

Optimization Algorithm for Solving Economic Dispatch Problem. In Advanced Control & Optimization Paradigms for Energy System Operation and Management (pp. 137-164). River Publishers.

Oyewola, D. O., Kehinde, T. O., Akinwunmi, S. A., & Abdulrahim, A.-M. (2025). Stock

market prediction with optimized PLSTM-AL in smart urban cities. Finance Research Open, 1(3), 100019. https://doi.org/10.1016/j.finr.2025.100019.

Oyewola, D. O., Akinwunmi, S. A., & Omotehinwa, T. O. (2024). Deep LSTM and LSTM-

attention Q-learning–based reinforcement learning in oil and gas sector prediction. Knowledge-Based Systems, 284, 111290. https://doi.org/10.1016/j.knosys.2023.111290

Oyewola, D. O., Akinwunmi, S. A., & Taura, J. J. (2026). Predictive Multivariate Financial

Time series in Nigerian Stock Market Using Hybrid Runge Kutta Optimization Dual Attention Long Short-Term Memory (RUN-DA-LSTM). NIPES - Journal of Science and Technology Research, 8(1), 1–32. https://doi.org/10.37933/nipes/8.1.2026.2043.

Oziegbe, T. E., Edje, A. E., & Akazue, M. (2026). Enhanced gated recurrent unit deep

learning model for vehicular networks anomaly-based intrusion detection. FUDMA Journal of Sciences (FJS), 10(2), 38–44. https://doi.org/10.33003/fjs-2026-1002-4351.

Salo, A., Doumpos, M., Liesiö, J., & Zopounidis, C. (2024). Fifty years of portfolio

optimization. European Journal of Operational Research, 318(1), 1–18. https://doi.org/10.1016/j.ejor.2023.12.031.

Sezer, OB, Gudelek, MU, & Ozbayoglu, AM (2020). Financial time series forecasting with

deep learning: A systematic literature review: 2005–2019. Applied soft computing, Elsevier, https://www.sciencedirect.com/science/article/pii/S1568494620301216.

Whitley, D., 1994. A genetic algorithm tutorial. Statistics and computing, 4(2), pp.65-85.

Xiao, H. (2025). Enhanced separation of long-term memory from short-term memory on top

of LSTM: Neural network-based stock index forecasting. PLoS ONE, 20(6), e0322737. https://doi.org/10.1371/journal.pone.0322737.

Yan, H, & Ouyang, H (2018). Financial time series prediction based on deep learning.

Wireless Personal Communications, Springer, https://doi.org/10.1007/s11277-017-5086-2.

Yang, S. (2021). A novel study on deep learning framework to predict and analyze the

financial time series information. Future Generation Computer Systems, 123, 205–216. https://doi.org/10.1016/j.future.2021.05.006.

Zhang, C., Sjarif, N. N. A., & Ibrahim, R. (2024). Deep learning models for price forecasting

of financial time series: A review of recent advancements (2020–2022). Wiley Interdisciplinary Reviews: Data Mining and Knowledge Discovery, e1519. https://doi.org/10.1002/widm.1519.

Zhang, Y., Yan, B., & Aasma, M. (2020). A novel deep learning framework: Prediction and

analysis of financial time series using CEEMD and LSTM. Expert Systems with Applications, 159, 113609. https://doi.org/10.1016/j.eswa.2020.113609.

Zhao, W., Zhang, Z., Khodadadi, N., & Wang, L. (2025). A deep learning model coupled with

metaheuristic optimization for urban rainfall prediction. Journal of Hydrology, 651, 132596. https://doi.org/10.1016/j.jhydrol.2024.132596

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 David Opeoluwa Oyewola, Sulaiman Awwal Akinwunmi, Joel John Taura

This work is licensed under a Creative Commons Attribution 4.0 International License.