AN IMPROVED MODEL FOR THE CLASSIFICATION OF CREDIT RISK USING HYBRID DEEP LEARNING APPROACH

DOI:

https://doi.org/10.33003/fjs-2026-1005-4709Keywords:

Credit Risk, Improved Model, Deep Learning,, DNN-based ModelAbstract

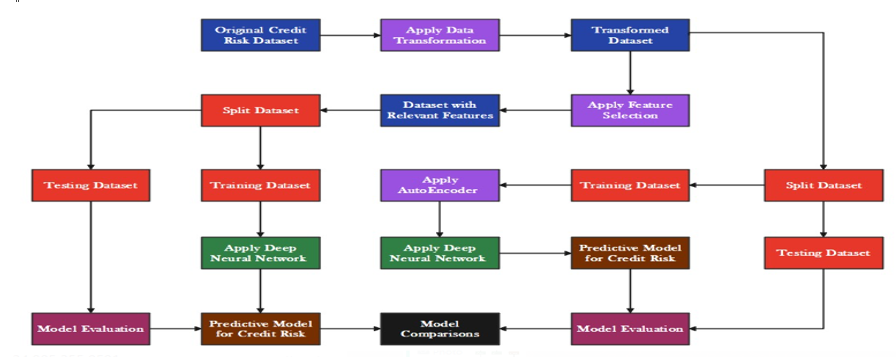

This study identified credit risk factors in the Nigerian banking sector and developed a hybrid deep learning model to improve credit facility engagements. Both secondary and primary datasets were employed. Secondary data were sourced from selected commercial banks and peer-reviewed publications, while primary data were gathered through Key Informant Interviews (KII) with experienced commercial bankers. Categorical features underwent data transformation, and feature importance was assessed using mutual information, which informed the generation of a reformed dataset. A Hybrid Deep Learning classification model was formulated and simulated using varying proportions of the hold-one-out method via Google Colaboratory. Model performance was evaluated based on accuracy, true positive rate, false positive rate, and precision. Six key features were identified as most relevant to credit risk classification: monthly income, annual income, amount invested monthly, outstanding debt, equated monthly installments, and type of loan. The DNN-based model trained on these features achieved a prediction accuracy of 99.9%, significantly reducing redundancy across the original 23 features and cutting processing time. Furthermore, the Hybrid model (combining an AutoEncoder with a Deep Neural Network) outperformed a standalone DNN-based model by 46.8%. The study concluded that selecting relevant features for predictive modelling tasks reduces model complexity, simulation time, and memory usage, collectively contributing to improved performance. These findings offer a practical framework for enhancing credit risk assessment in the Nigerian banking sector through intelligent, efficiency-driven machine learning approaches.

References

Abdelmoula, A. (2015). Bank Credit Risk Analysis with k-Nearest Neighbour Classifier: Case of Tunisian Banks. Accounting and Management Information Systems, 14(1), 79-105.

Anita, C. (2008). Credit risk assessment: Prescription for Indian Banks. In A. Silva, Credit Risk Models: New Tools of CRedit Risk Management (pp. 3-15). Hyderabad, India: The ICFAI University Press.

Bennett, J., Bohoris, G., Aspinwall, E., and Hall, R. (1996). Risk analysis techniques and their application to software development. European Journal of Operational Research, 95(3), 467-475.

Brkic, S., Hodzic, M., and Dzanic, E. (2017). Fuzzy Logic Model of Soft Data Analysis for Corporate Client Credit Risk Assessment in Commercial Banking. Fifth Scientific Conference with International Participation “Economy of Integration” ICEI 2017 (pp. 1-10). SSRN.

Chi, G., Uddin, M., Abedin, M., and Yuan, K. (2019). Hybrid Model for Credit Risk Prediction: An Application of Neural Network Approaches. International Journal on Artificial Intelligence Tools, 28(5).

Darwish, N., and Abdelghany, A. (2016). A Fuzzy Logic Model for Credit Risk Rating of Egyptian Commercial Banks. International Journal of Computer Science and Infromation Security, 14(2), 11-18.

Hasan, I., Elghareeb, H., Farahat, F., and AboElfotouh, A. (2021). A Proposed Fuzzy Model for reducing the Risk of Insolvent Loans in the CRedit Sector as Applied in Egypt. International Journal of Fuzzy Logic and Intelligent Systems, 21(1), 66-75. doi:http://dx.doi.org/10.5391/IJFIS.2021.21.1.66

Kin, T., Aizam, A., Hasan, S., Ariffin, A., and Mahat, N. (2021). Bankruptcy Prediction Model with Risk Fcators using Fuzzy Logic Approach. Journal of COmputing Research and Innovation, 6(2), 104-113. Retrieved from https://doi.org/10.24191/jcrinn.v6i2.220

Manab, N., Theng, N., and Md-Rus, R. (2015). The Determinants of Credit Risk in Malaysia. Procedia - Social and Behavioral Sciences, 172, 301-308.

Mohammed, A., and Salama, A. (2013). A Fuzzy Logic Based Model for Predicting Commercial Banks Financial Failure. International Journal of Computer Applications, 79(11), 1-12.

Moscato, V., Picariello, A., and Sperli, G. (2021). A Benchmark of Machine Learning Approaches for CRedit Score Prediction. Expert Systems with Applications, 165-173. doi:10.1016/j.eswa.2020.113986.113986

Munkhdalai, L., Munkhdalai, T., Namsrai, O.-E., Lee, J., and Ryu, K. (2019). An Empirical Comparison of Machine Learning Methods on Bank Client Credit Assessments. Sustainability, 11(3), 699-713. Retrieved from https://doi.org/10.3390/su11030699

Nyangena, B. (2019). Consumer CRedit Risk modeling using Machine Learning Algorithms: A Comparative Approach. Strathmore University, Department of Mathematics. Strathmore University.

Salihu, A., and Shehu, V. (2020). : A Review of Algorithms for Credit Risk Analysis. : Proceedings of the ENTRENOVA - ENTerprise REsearch InNOVAtion Conference (pp. 134-146). Zagreb: Society for Advancing Innovation and Research in Economy.

Shi, S., Tse, R., Luo, W., D'Addona, S., and Pau, G. (2022). Machine Learning-Driven Credit Risk: A Systematic Review. Neural Computing and Applications, 34, 14327-14339. Retrieved from https://doi.org/10.1007/s00521-022-07472-2

Tian, Z., Xiao, J., Feng, H., and Wei, Y. (n.d.). Credit Risk Assessment based on Gradient Boosting Decision Tree. Procedia Computer Science, 174, 150-160. doi:http://dx.doi.org/10.1016/j.procs.2020.06.070

Wandmacher, R., Sturm, C., Weber, P., and Kuhn, P. (2022). Artificial Intelligence in Business Management: A Literature Review on AI Applications on Risk Assessment in the Financial Industry. American Journal of Management Science and Engineering, 7(4), 59-68. doi:10.11648/j.ajmse.20220704.14

Wang, L., and Song, H. (2022). E-Commerce Credit Risk Assessment based on Fuzzy Neual Network. Advances in Computational Intelligence Techniques for Next Generation Internet of Things, 1-13.

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 Emmanuel Oladimeji Ayodele, Temitope Folasade Sholanke, Peter Adebayo Idowu

This work is licensed under a Creative Commons Attribution 4.0 International License.