DISTRIBUTIONAL PROPERTIES OF NAIRA EXCHANGE RATE VOLATILITY: AN INVERSE GAMMA PERSPECTIVE

DOI:

https://doi.org/10.33003/fjs-2026-1001-4535Keywords:

Exchange rate volatility, Inverse gamma distribution, Heavy-tailed volatility, Naira exchange rate, Tail risk, Emerging marketsAbstract

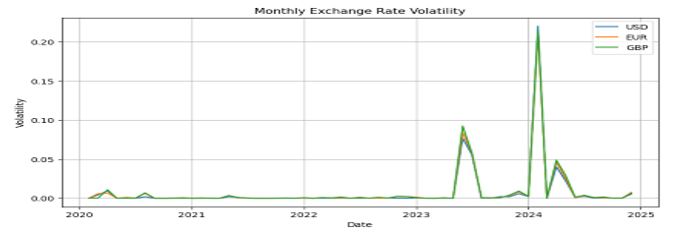

This study investigates the distributional properties of monthly exchange rate volatility of the Nigerian Naira, with particular emphasis on inverse gamma behavior. Monthly exchange rate data for the Naira against the US Dollar (USD), Euro (EUR), and Pounds Sterling (GBP) from January 2020 to December 2024 are analyzed. Exchange rate volatility is proxied using squared logarithmic returns. Descriptive statistics indicate that the volatility series are strictly positive, highly right-skewed, and extremely leptokurtic, with skewness values exceeding 5 and kurtosis values above 30 for all currencies, confirming pronounced heavy-tailed behavior. The inverse gamma distribution is estimated using maximum likelihood techniques, and goodness-of-fit is assessed using the Kolmogorov–Smirnov test and graphical diagnostics. The Kolmogorov–Smirnov test rejects the null hypothesis of an exact inverse gamma distribution for all currency pairs; however, quantile–quantile plots show strong alignment between empirical and theoretical quantiles in the upper tail. Comparative volatility analysis reveals that the Naira–Pounds Sterling exchange rate exhibits the highest volatility, followed by the Naira–Euro and the Naira–US Dollar exchange rates. Although alternative distributions such as the gamma and lognormal achieve higher log-likelihood values, the inverse gamma distribution remains useful for capturing extreme exchange rate volatility, which is of primary interest in financial risk analysis.

References

Andersen, T. G., & Bollerslev, T. (1998). Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International Economic Review, 39(4), 885–905. https://doi.org/10.2307/2527343

Andersen, T. G., Bollerslev, T., Diebold, F. X., & Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica, 71(2), 579–625. https://doi.org/10.1111/1468- 0262.00418

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307–327. https://doi.org/10.1016/0304-4076(86)90063-1

Chib, S., Omori, Y., & Asai, M. (2006). Bayesian analysis of stochastic volatility models with heavy-tailed distributions. Journal of Econometrics, 135(2), 263–290. https://doi.org/10.1016/j.jeconom.2005.07.002

Cont, R. (2001). Empirical properties of asset returns: Stylized facts and statistical issues. Quantitative Finance, 1(2), 223–236. https://doi.org/10.1088/1469-7688/1/2/304

Embrechts, P., Klüppelberg, C., & Mikosch, T. (1997). Modelling extremal events for insurance and finance. Springer.

Engle, R. F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4), 987–1007. https://doi.org/10.2307/1912773

Frankel, J. A., & Rose, A. K. (1996). Currency crashes in emerging markets: An empirical treatment. Journal of International Economics, 41(3–4), 351–366. https://doi.org/10.1016/S0022-1996(96)01441-9

Kim, S., Shephard, N., & Chib, S. (1998). Stochastic volatility: Likelihood inference and comparison with ARCH models. Review of Economic Studies, 65(3), 361–393. https://doi.org/10.1111/1467-937X.00050

Kuhe, D. A., Torruam, J. T., & Yaweh, B. I. (2025). Stock market prices and foreign exchange rate interactions in Nigeria: Evidence from cointegrated VAR model. FUDMA Journal of Sciences, 9(7), 304–314. https://doi.org/10.33003/fjs-2025-0907-3804

Mandelbrot, B. (1963). The variation of certain speculative prices. Journal of Business, 36(4), 394–419. https://doi.org/10.1086/294632

Obstfeld, M., & Rogoff, K. (1996). Foundations of international macroeconomics. MIT Press.

Olowe, R. A. (2009). Modelling Naira/Dollar exchange rate volatility: Evidence from GARCH and asymmetric models. International Review of Business Research Papers, 5(3), 377–398.

Omotosho, B. S., & Doguwa, S. I. (2012). Understanding the dynamics of inflation volatility in Nigeria: A GARCH perspective. CBN Journal of Applied Statistics, 3(2), 51–74.

Salisu, A. A., & Fasanya, I. O. (2013). Modelling oil price volatility with structural breaks. Energy Policy, 52, 554–562. https://doi.org/10.1016/j.enpol.2012.10.003

Taylor, S. J. (1986). Modelling financial time series. John Wiley & Sons.

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2026 Babatunde Sunday Elijah

This work is licensed under a Creative Commons Attribution 4.0 International License.