VOLATILITY MODELLING OF NIGERIA CONSUMER STAPLES STOCKS IN THE PERIOD OF GLOBAL ECONOMIC CRISIS (2012–2024)

DOI:

https://doi.org/10.33003/fjs-2025-0910-3842Keywords:

Consumer staple goods, Component GARCH, Power GARCH, Economic crisis, NigeriaAbstract

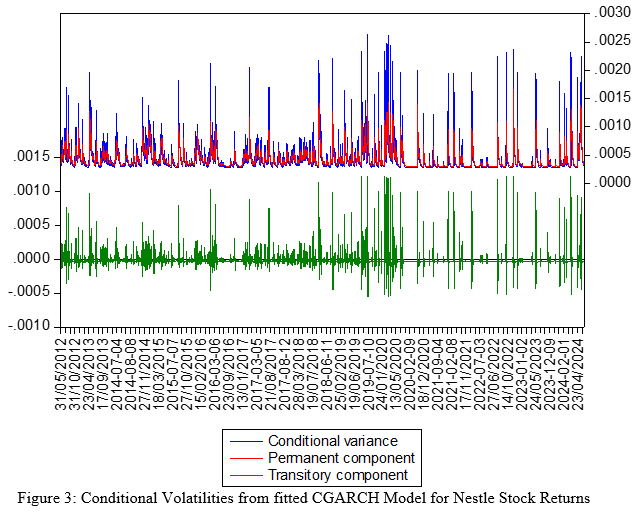

The period from 2012 to 2024 was faced with significant economic events and policy shifts in Nigeria, including fluctuations in oil prices, movements in consumer staple stocks, changes in government policies, currency devaluations, and the global impact of the COVID-19 pandemic. This study focuses on consumer staple stocks, specifically Nestle Nigeria Plc and Presco Plc which are the two leading consumer staple stocks listed on the Nigerian stock market. An empirical, quantitative time-series design using daily closing prices of these stocks of 2,809 observations per stock from 5th March 2012 to 11th June, 2024 were sourced and analysed. The analysis employs descriptive statistics, stationarity tests, and ARCH/GARCH family models to examine the return dynamics of Nestle Nigeria Plc and Presco Plc. The results reveal that Nestle Nigeria Plc had an average return of 0.000271 with a standard deviation of 0.020553, while Presco Plc recorded a higher average return of 0.001213 and exhibited greater volatility with a standard deviation of 0.027072. The Augmented Dickey-Fuller test confirmed that both stock return series were stationary at first differencing. The presence of significant ARCH effects in both series justified the application of GARCH-type models. Among the models evaluated, the Component GARCH (CGARCH) model provided the best fit for Nestle Nigeria Plc, while the Power ARCH (PARCH) model was most suitable for capturing the volatility of Presco Plc, based on the lowest AIC and SIC values. The study recommends further refinement of volatility models and the implementation of policy measures aimed at stabilizing stock price...

References

Aborisade, O., Carpio, C. E., &Boonsaeng, T. (2024). Food demand estimation from consumption and expenditure data: Meat demand in Nigeria. Agricultural and Resource Economics Review, 53(2), 144–162. https://doi.org/10.1017/age.2023.34

Adeyeye, P. O., Aluko, O. A., &Migiro, S. O. (2018). The global financial crisis and stock price behaviour: Time evidence from Nigeria. Global Business and Economics Review, 20(3), 373–387. https://doi.org/10.1504/GBER.2018.091712

Ajibade, T. B., Ayinde, O. E., & Abdoulaye, T. (2020). Food price volatility in Nigeria and its driving factors: Evidence from GARCH estimates. International Journal of Food and Agricultural Economics, 8(4), 367–380.

Atobatele, O. (2023). Foreign direct investment: A case study of Nestle S.A. in Nigeria. Modern Economy, 14, 825–832. https://doi.org/10.4236/me.2023.146044

Ayanlowo E. A., Oladapo D. I., Madu P. N. and Obadina G. O. (2025). The Econometric Impact of Petroleum Subsidy Removal on the Nigerian Economy. (2025). Fudma Journal of Sciences, 9(7), 195-200. https://doi.org/10.33003/fjs-2025-0907-3775

Central Bank of Nigeria. (2024, March). Macroeconomic outlook: Price discovery for economic stabilisation. Abuja, Nigeria.

Čermák, M., Malec, K., &Maitah, M. (2017). Price volatility modelling – Wheat: GARCH model application. Agris on-line Papers in Economics and Informatics, 9(4), 1–10.

Egea, J. A., García, M. R., & Vilas, C. (2023). Dynamic modelling and simulation of food systems: Recent trends and applications. Foods, 12(3), 557. https://doi.org/10.3390/foods12030557

Emenike, K. O. (2010, January 15). Modelling stock returns volatility in Nigeria using GARCH modelsMunich Personal RePEc Archive. (MPRA Paper No. 22723, pp. 1–19). https://mpra.ub.uni-muenchen.de/22723/

Emenike, Kalu O. (2010): Modelling Stock Returns Volatility In Nigeria Using GARCH Models. Published in: Proceeding of International Conference on Management and Enterprice Development, EbitimiBanigo Auditorium, University of Port Harcourt - Nigeria, 1 (4), 5-11.

Jatau, M., Chiawa, M. A., &Kuhe, D. A. (2018). Modeling stock returns volatility in Nigeria: Applications of GARCH family models. Asian Journal of Economics, Business and Accounting, 9(1), 1–12. https://doi.org/10.9734/AJEBA/2018/39861

Mohammed, T., Umar, Y. H., & Adams, S. O. (2022). Modeling the volatility for some selected beverages stock returns in Nigeria (2012–2021): A GARCH model approach. Matrix Science Mathematic, 6(2), 41–51. https://doi.org/10.26480/msmk.02.2022.41.51

Onunaka, U. F., &Okezie, S. (2024). Impact of stock price flakiness on development of Nigerian Exchange Group. Certified National Accountant Journal, 32(1), 70–93. https://doi.org/10.70518/cnaj.v32i1.05

Presco Plc. (2023). Annual report, consolidated and separate financial statements for the year ended 31. https://www.presco-plc.com

Salami, A., &Olasehinde, T. (2021). Stock price volatility modelling with regimes in conditional mean and variance. Asian Journal of Economics, Business and Accounting, 21(2), 123–131. https://doi.org/10.9734/ajeba/2021/v21i230355

Salami, A., & Olasehinde, T. (2021). Stock price volatility modelling with regimes in conditional mean and variance. Asian Journal of Economics, Business and Accounting, 21(2), 123–131. https://doi.org/10.9734/ajeba/2021/v21i230355

Samson, T. K., Onwukwe, C. E., &Enang, E. I. (2020). Modelling volatility in Nigerian stock market: Evidence from skewed error distributions. International Journal of Modern Mathematical Sciences, 18(1), 42–57. http://www.modernscientificpress.com/Journals/ViewArticle.aspx?JMPID=23

Schwert, G.W. (1989) Why Does Stock Market Volatility Change over Time? Journal of Finance, 44, 1115-1153. http://dx.doi.org/10.1111/j.1540-6261.1989.tb02647.x

Setiawati, I., Ardiansyah, &Taufikurohman, R. (2021). Price volatility of staple food using ARCH-GARCH model. IOP Conference Series: Earth and Environmental Science, 653(1), 012146. https://doi.org/10.1088/1755-1315/653/1/012146

Sokpo, J., Iorember, P., & Usar, T. (2017). Inflation and stock market returns volatility: Evidence from the Nigerian Stock Exchange 1995Q1–2016Q4: An E-GARCH approach. Munich Personal RePEc Archive (MPRA Paper No. 85656,pp. 1–19). https://mpra.ub.uni-muenchen.de/85656/

Tanimu M., and Yahaya H. U. (2024). Modelling the Volatility of Stock Returns in Some Selected African Countries. Socio Economy and Policy Studies, 4(1): 60-77. Doi: 10.26480/seps.01.2024.44.51

Taylor, S.J. (1986) Modelling Financial Time Series. John Wiley and Sons, Ltd., Chichester.

Downloads

Published

Issue

Section

Categories

License

Copyright (c) 2025 Godwin Arunsi Iro, Haruna Umar Yahaya

This work is licensed under a Creative Commons Attribution 4.0 International License.